By Jackson Dille and Whitney Afonso

Questions for Practitioners

- How is the shift towards sales taxes affecting fiscal equity across North Carolina counties?

- How has North Carolina’s local sales tax redistribution policy impacted the difference in per capita sales tax dollars between urban and rural counties?

- What lessons does North Carolina’s experience offer for designing equitable fiscal policies in regions with stark urban-rural divides?

Introduction

Local sales taxes (LSTs) have become an increasingly important revenue source for local governments, growing from 7% of total local tax revenues in 1977 to 13% by 2020, with collections surpassing $100 billion. Their popularity stems from their flexibility, political palatability, and ability to diversify revenue streams while offering property tax relief and shifting the tax burden to non-residents. However, the benefits are unevenly distributed, as some jurisdictions experience tax “exportation”—benefiting from non-resident spending—while others suffer from “tax leakage” when residents shop elsewhere. These dynamics have led to significant disparities in sales tax revenues between retail-rich and retail-poor communities.

To address these inequities, North Carolina implemented a redistribution policy in 2017 that pooled a portion of local sales tax revenue at the state level and redistributed it based on a formula designed to reflect both place of sale and population. Then-Senate Majority Leader Harry Brown described the initiative as a way to ensure “all North Carolina counties benefit from tax dollars their own citizens pay.” While the motivation behind the policy is clear, its real-world impact had not been evaluated until recently. The study reviewed here is the first to assess whether this kind of policy meaningfully reduces fiscal inequities tied to sales tax revenue and whether it is well-designed to adapt over time.

Background of LST in North Carolina

In North Carolina, LSTs represent the second-largest source of revenue for counties, trailing only property taxes. However, not all counties have equal ability to generate this revenue. Tax leakage—when residents shop in neighboring counties, particularly from rural to urban areas—creates fiscal challenges for rural communities lacking commercial infrastructure. Urban counties, with more retail activity and larger visitor flows, benefit disproportionately. As a result, rural counties often face lower per capita LST collections and greater challenges funding essential services like education and public safety.

To correct this imbalance, the General Assembly enacted a reform in FY2017 that aimed to redistribute part of the LST revenue more equitably. Under this system, each county contributes a share of its LST collections into a state-managed pool. Revenues from Articles 39, 40, and 42 are included, and then redistributed to counties based on fixed allocation percentages derived from a projected 50–50 split between point-of-sale and per capita distributions. This policy sought to strengthen counties with weaker sales tax bases—typically rural areas—by supplementing their revenue and mitigating the impact of tax leakage. While well-intentioned, the fixed nature of these allocation percentages and their lack of alignment with actual county contributions have introduced challenges in implementation.

Impact of the Revenue Sharing Pool

To evaluate the policy’s effectiveness, researchers used financial data from the North Carolina Department of Revenue and categorized counties as urban or rural. In theory, rural counties with smaller LST bases would benefit the most, while urban counties with larger bases would contribute more than they receive. However, the actual outcomes proved more complex. In FY2017, approximately 75% of rural counties and 50% of urban counties were net beneficiaries. Some rural counties were net contributors, while some urban counties gained more than they paid in. This divergence is partially due to the imperfect alignment between rural/urban designations and actual tax base size. Some rural counties, despite their classification, had relatively strong retail sectors, and some urban counties had weaker ones.

A central issue is that the policy’s allocation formula does not factor in each county’s contribution to the pool. Instead, it relies on fixed distribution percentages based on projections from 2015. As a result, counties with higher contributions may not see proportional returns, and recipient counties may receive less than their level of need or contribution would suggest. In fact, 12 of the 33 counties with net negative revenues in FY2017 received less revenue than they contributed even though they were intended to be net recipients..

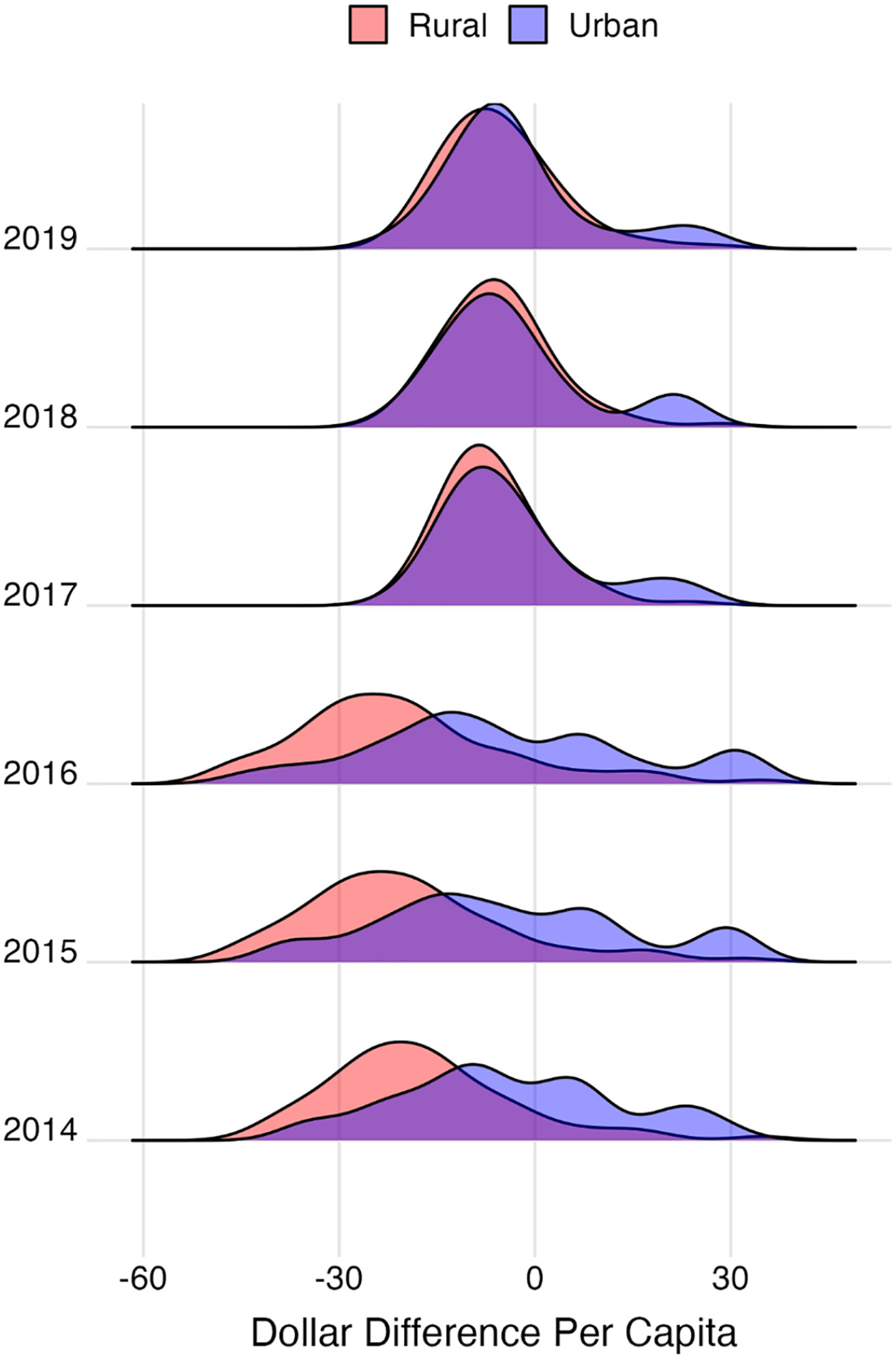

Still, the policy’s redistributive effect remains evident, especially when measured relative to per capita LST revenue. Urban counties with high sales tax capacity per capita experienced modest losses—median losses around 2.9%—while rural counties with low capacity gained significantly, with some seeing increases as high as 58%. Comparing actual revenue to a hypothetical 50–50 target also revealed that, post-policy, the gap between actual and intended revenue narrowed, particularly among rural counties. Over time, however, these gains have started to erode. As certain counties continue to grow economically, disparities in per capita LST revenue have begun to widen again, reflecting the policy’s limited adaptability. Figure 1 shows difference in LST dollars per capita across urban and rural counties over time.

Figure 1: Per Capita Dollar Difference Between Urban and Rural Counties

Source: Afonso et al. 2024

Conclusion

North Carolina’s LST redistribution policy represents a thoughtful effort to reduce fiscal disparities and address the challenge of tax leakage between counties. Many rural jurisdictions have meaningfully benefited, and the policy has helped align actual revenues more closely with a population-adjusted benchmark. At the same time, certain design features may limit the policy’s long-term effectiveness. Notably, the use of fixed allocation percentages—based on projections made in 2015—does not reflect counties’ actual contributions to the revenue pool or shifts in local economic conditions over time.

While the policy successfully narrowed revenue disparities in its early years, its static structure may benefit from future refinements to sustain that progress. Updating allocation percentages periodically, incorporating contributions into the formula, or adopting a broader definition of fiscal capacity (including other local revenue sources like property taxes or fees) could enhance both equity and responsiveness. North Carolina’s experience offers important insights for other states pursuing similar reforms: effective revenue-sharing policies can provide meaningful support to communities with lower fiscal capacity, but they are most impactful when designed to evolve alongside changing economic and demographic landscapes.

Finally, it is also critical to consider the cost to the counties that are the beneficiaries of tax leakage (those that import tax dollars) from those non-resident visitors. Those who commute, travel, and shop in other jurisdictions also consume services and benefit from those public dollars. As the state (and others) continue to consider what is fair, perhaps measuring the difference between the cost incurred by the counties that import sales tax dollars and the amount that they receive in surplus dollars is a worthwhile exercise. Ultimately, careful consideration of policy goals and their impacts is warranted. In the case of GS 105-524, the state set out to correct for tax leakage and they were largely successful in achieving that goal.

Full article: Afonso, Whitney, Alex Combs, and Christian Buerger. “Plugging the Tax Leak: An Analysis of North Carolina’s Local Sales Tax Redistribution Policy.” State and Local Government Review 56.1 (2024): 76-90.