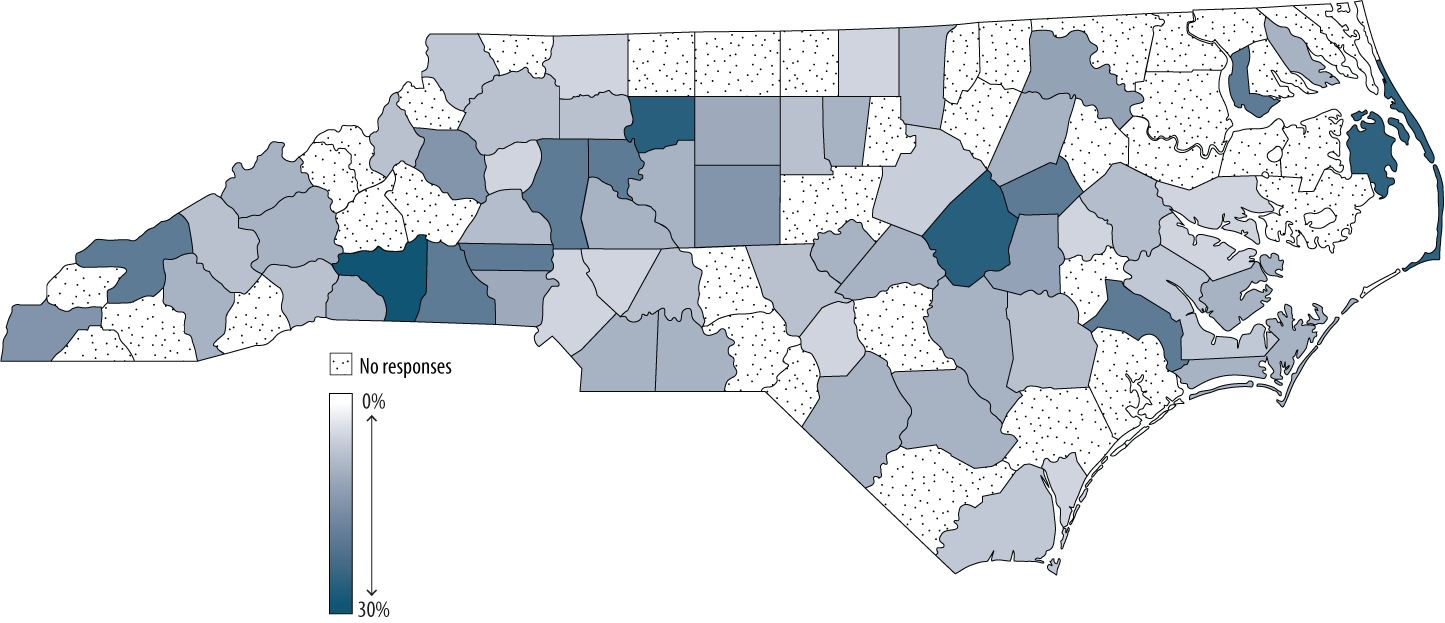

Recently the North Carolina League of Municipalities (NCLM) and the North Carolina Local Government Budget Association (NCLGBA) partnered on a survey of county and municipal governments across the state to better understand how local governments are budgeting for FY21. There are 142 responses. 29 are from counties and 113 are from municipalities. See the map below to see the number of jurisdictions from each county area (total of the county and municipal responses).

The Impact on Revenues

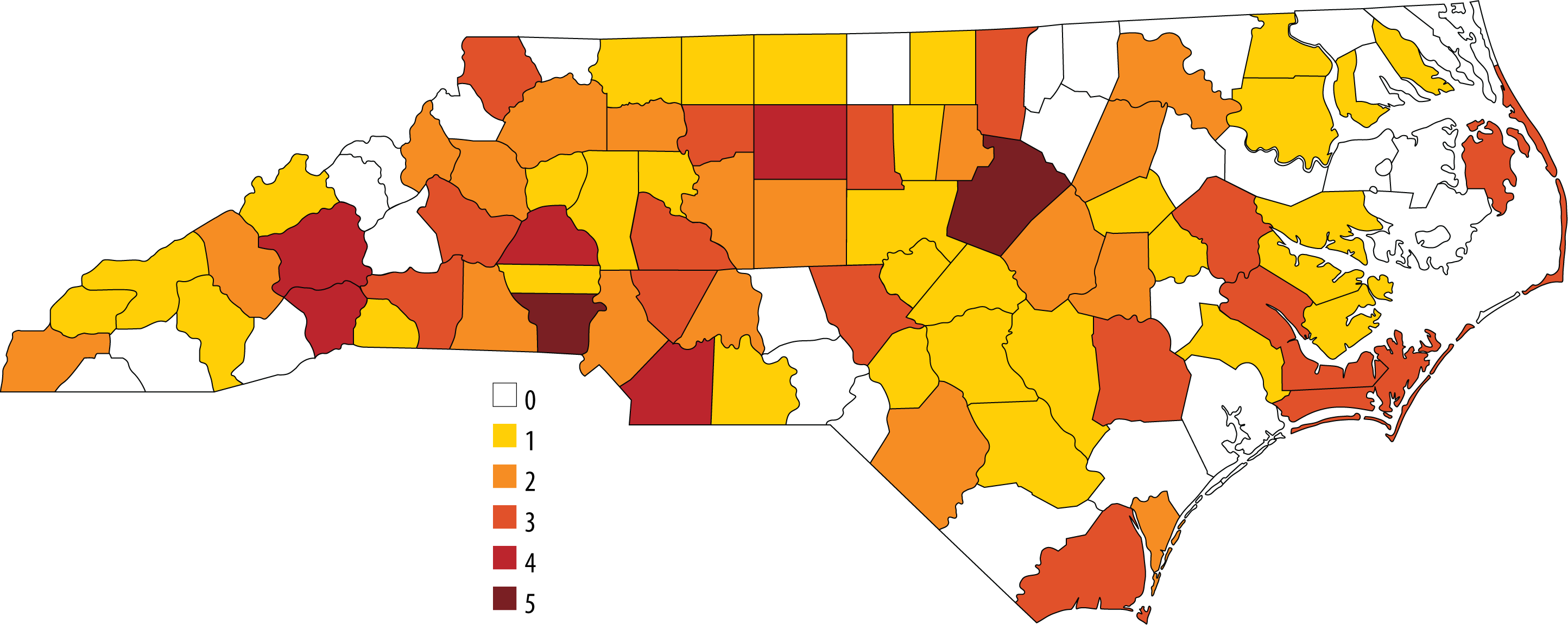

The results suggest that, not surprisingly, the industries being most impacted are tourism, restaurants, and retail. Most respondents reported that real estate, construction, and manufacturing sectors were stable if not growing. However, despite the fact that some sectors have so far been shielded, the majority of jurisdictions report expecting General Fund shortfalls for FY21, 92% in fact. Almost a fifth of respondents are anticipating a General Fund shortfall of greater than 10%. The map below shows the distribution of those jurisdictions expecting a general fund shortfall and by how much. Please note that is a jurisdiction reported “Unsure” it was coded as a “No” for expecting a shortfall and to create the average shortfall the higher end of the range was used.

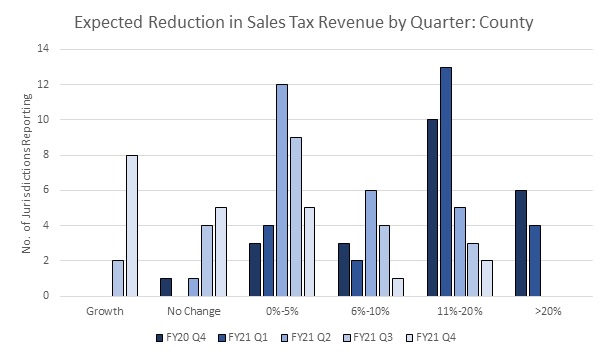

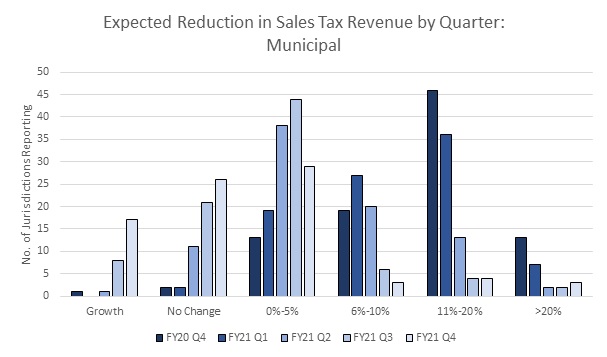

The county areas that are anticipating the largest shortfalls are Johnston, Dare, Rutherford, Jones, and Forsyth. With the exception of Forsyth, it is rural county areas. This may reflect not just the broader economies, but also the dependence on different streams of revenue. Respondents, as anticipated, are expecting some revenue sources to be more impacted than others. Sales taxes are expected to be being hit hard. In fact, while we do not have the numbers yet, it is clear that they are already being hit hard. Below are two tables, one for county and one for municipalities showing the quarterly expectations of revenue shortfalls from the sales tax. It shows that while most jurisdictions believe that the last FY20 Q4 and FY21 Q1 will see substantial shortfalls, many are optimistic that by FY21 Q2 the impact of the current COVID-19 pandemic will have only a minor impact on sales taxes.

Occupancy taxes and in some cases, property taxes are expected to be negatively impacted as well. The majority of municipalities are anticipating shortfalls in occupancy tax revenue for the remainder of FY20 and slightly less dramatic reductions in revenues for FY21.

Most jurisdictions are anticipating stability or even growth in property taxes. This is expected since the property tax base was finalized in January before the effects of COVID-19 were felt in the United States. However, there are some still anticipating declines. The survey provided space for respondents to comment on why and those who chose to, typically suggested that it is because they believed that collection rates may decline.

Other revenues highlighted by comments were typically about reductions in revenues from 1) utilities, 2) investment and interest earnings, and 3) recreation. There were also questions around intergovernmental transfers (IGTs) from the state and federal government. Most jurisdictions responding did not have a lot of certainty about how these IGTs may be impacted, but those who were willing to speculate noted that they believed that they would be stable (though more reported expecting declines than increases).

The Impact on Expenditures

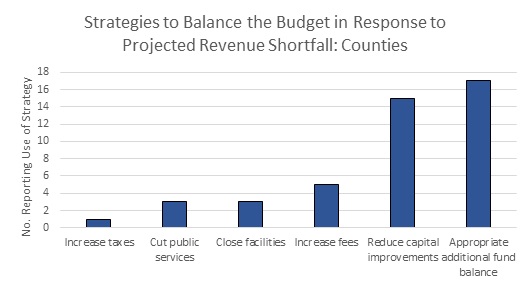

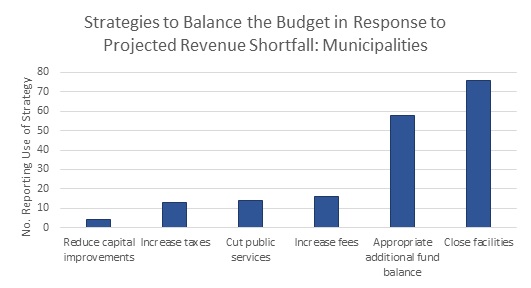

The projected revenue shortfalls are creating the need for local governments to consider many strategies to get their budgets into balance. Overall, the most common strategy reported was appropriating fund balance and the least common one was to increase taxes.

The strategies reported by counties and municipalities did vary though. Counties also reported relying heavily on reducing capital expenditures and increasing fees. Municipalities relied most heavily on closing facilities, then appropriating fund balance, and then increasing fees. Very few municipalities reported an intention to reduce capital expenditures.

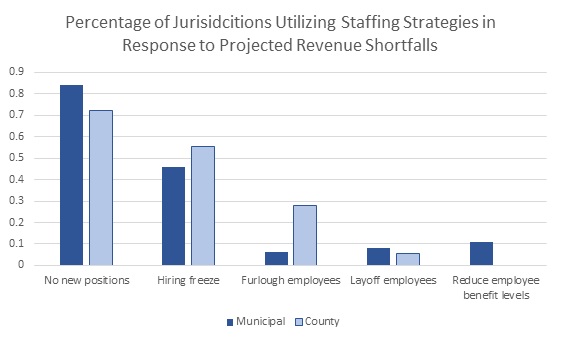

Additionally, counties and municipalities both reported the reductions in revenues were going to impact staffing decisions. The majority of respondents report not budgeting for any new positions and almost half report instituting a hiring freeze. Counties were more likely to furlough employees and only municipalities reported considering reducing employee benefits.

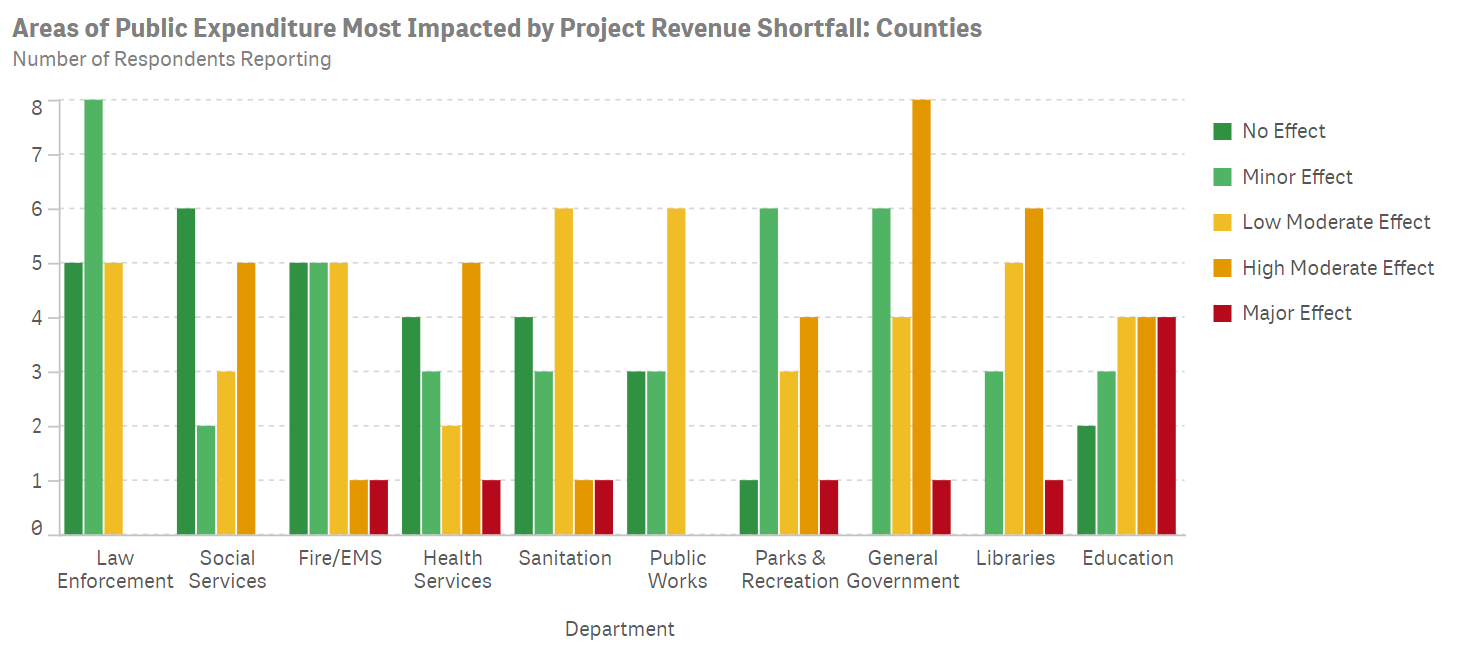

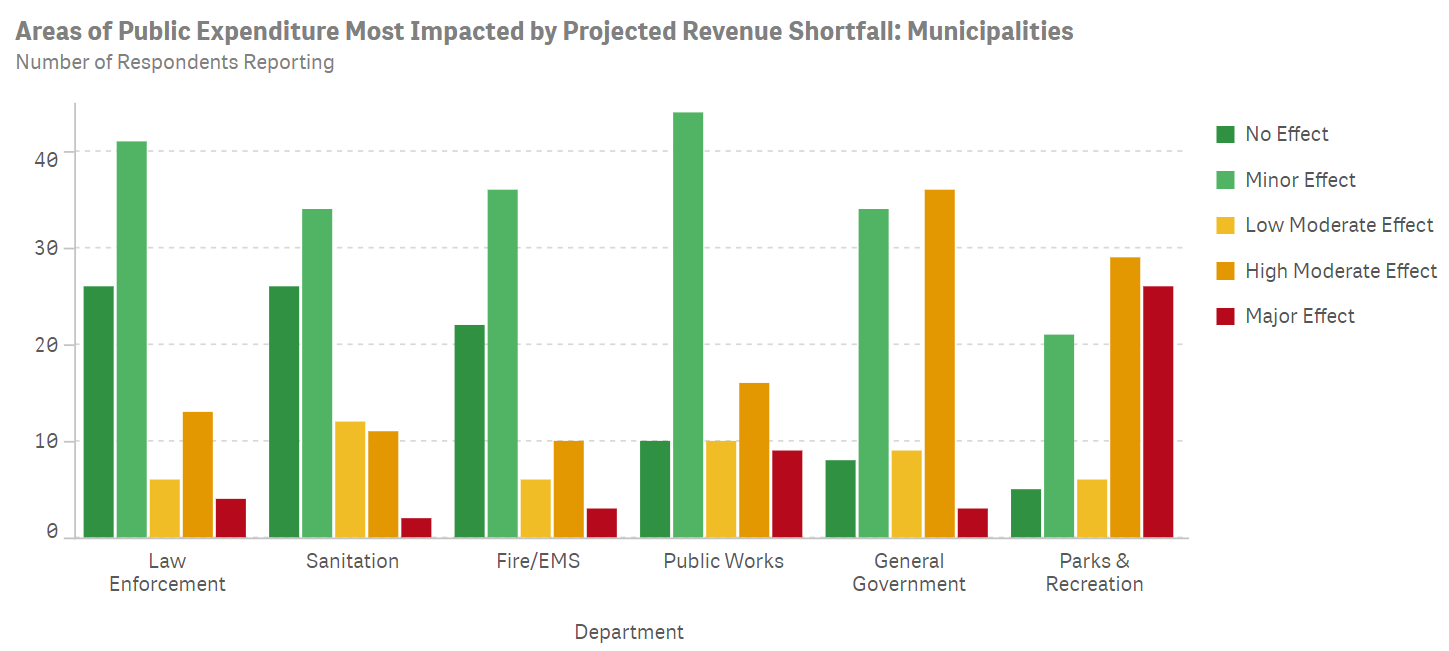

Lastly, some departments are reported to bear a larger portion of any decreases to the budget. Not surprisingly, law enforcement and fire and EMS are largely spared, whereas general government and parks and recreation are expected to both be moderately or highly impacted. Interestingly, for counties, education is also expected to be impacted greatly. Whether this is subsidies to the operating costs or areas of capital delays is unclear.

What does the scholarship say about how to best proceed with budgeting for FY21?

Well, the best practice is to smooth both expenditures and revenue policy, i.e. try and change as little as possible. Spend the money you had planned to spend and tax and fee at the rates you had planned… So how do you do that? Well in two primary ways. First, hope that you get a lot of federal and/or state support and IGTs. Of course, you have no control over that and it may not happen. Most of you, according to the survey, do not anticipate that happening. Second, use reserves. Many call fund balances “rainy day funds” (at the state level there are actually separate funds for economic downturn and emergencies). Well, it is raining. If your reserves are high enough, you can smooth both expenditures and revenues by relying on them more heavily. Of course, that is not the only function of local government fund balance and we do not know how long the economic downturn brought on by the pandemic is going to last…so you still want to be somewhat cautious about how much you spend it down.

So then, what is next best? Well, after you have decided how much fund balance is responsible to use, the literature suggests the next best option is to increase revenues temporarily and preferably not regressive ones (like the sales taxes or many fees).

One more recommendation from the literature: avoid cutting back on capital expenditures! Everyone, okay almost everyone, decreases capital expenditures during recessions and there can be long term negative impacts associated with that strategy. Additionally, often during times of recession it is much less costly to invest in capital because interest rates are lower and often contracts are for less.

Additional Resources:

Theory and Practice for Coping with Economic Downturns at the Local Level: Part I

Leave a Reply