Although there are no deaths to avenge in this story, it can be a tragedy to lower a business personal assessment when it is not warranted. Reducing a value, is a de facto exemption. It is an expense to the county. Accounts (parcels) with the highest value in local governments are quite often business personal property accounts. When a BPP assessment is reduced without proper reason, it can create de facto classifications. This means your largest taxpayers could be assessed at a lower assessment ratio than the smallest residential taxpayers. That doesn't sit well with me. There are certainly many variables to consider when faced with a request to lower an assessed value. Read on for this 5 act, I mean 5 question, blog post.

- Is your data correct? I’ve blogged here about the importance of data in real property appraisal. If the square footage or other property characteristics are incorrect, it doesn’t make sense to expect your mass appraisal models to give accurate values. Business personal property appraisals typically require the use of historical cost in the appraisal models. I promise if you input the wrong cost, you’ll get an incorrectly calculated value. If you get a request to make a reduction in BPP value, why would you even consider it before making sure the property characteristics (all the correct costs) are accurate? Has this taxpayer’s listing (return) ever been verified through cost reconciliation? If not, you do not have a basis to assume the data is correct. Since large business personal accounts many times comprise a jurisdiction's largest accounts overall, these issues have great impact. Please do not reduce a $100 million assessment if the costs used to arrive at that assessment could be understated substantially. Make sure your data is correct.

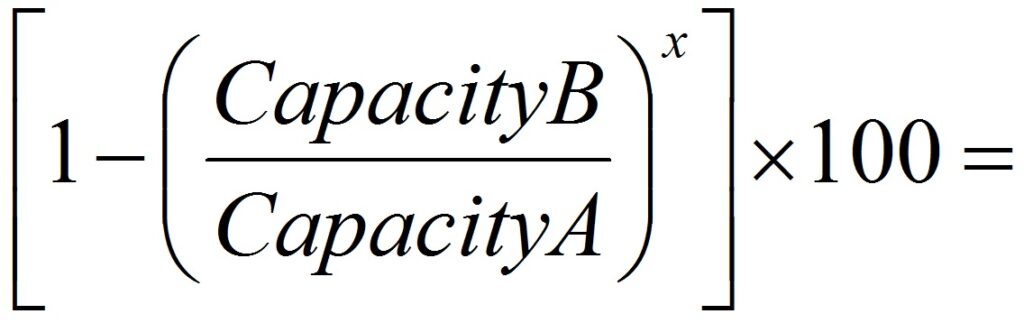

- Is the inutility penalty calculation used correctly? Is the what, doing what? Yes, some reductions in value are requested based on a formula that attempts to approximate economic obsolescence using a production to capacity formula.

[caption id="attachment_531" align="aligncenter" width="676"]

Email me for a spreadsheet that performs this calculation. Check all calculations provided to you in requests for reductions of value.[/caption]

Email me for a spreadsheet that performs this calculation. Check all calculations provided to you in requests for reductions of value.[/caption]If you accept a calculation using this formula as evidence of a 50% loss in value, but you don't understand the formula or the underlying business practices, that could be no different than lowering the assessed value of a 25-story downtown hotel by 50% without seeing it and verifying income and expense information. The inutility penalty formula and calculation can be a good way to calculate economic obsolescence, but only if you agree that the obsolescence exists in the first place. Length multiplied by width equals square footage, but only if the square footage exists. Sometimes there are very good reasons why production is less than capacity and those reasons do not always equal a loss in value. For example, careful thought is put into the designed capacity of a manufacturing process. These calculations are not guessed. The desired capacity is one expected to be needed at some point in the future. The economic principle of anticipation states that value is the present worth of anticipated future benefits. I have witnessed a request for a value reduction because capacity was double the current production level, but all of the activity surrounding the business indicated that the intent was to build capacity at that high level. Think about it. If expectation is that demand will grow, why would a manufacturing plant be constructed to meet exactly 100% of current demand? I've also seen a request for economic obsolescence, using this formula, that came at the same time as capital was pouring in for new equipment, all to increase capacity even more! That didn’t make sense. Why did they desire more than double their current production capacity, when the argument was that there was not enough demand to meet their capacity?

“The appraiser should determine the facts and circumstances and apply them as appropriate.” Valuing machinery and equipment: The fundamentals of appraising machinery and technical assets (3nd ed., p. 78). (2011). Washington, D.C.: American Society of Appraisers. “A plant operating at close to its full capacity doesn’t necessarily indicate that economic obsolescence is zero.”- ibid

I agree with that quotation, but take note that it infers a plant operating at close to the minimum of its capacity doesn’t necessarily indicate that economic obsolescence is high, or even exists at all. Finally, the exponent in the calculation (scale factor) changes the percent of economic obsolescence requested. Do you know the meaning of "scale factor" in an inutility calculation? Google does. Call me if you would like to discuss it!

- What is expected in years ahead? Related to my example above, if a business is increasing capacity while production is low, you should ask why. Likewise, if a business’s competition (the market) is expanding operations in the same area where the subject indicates a lack of demand, the lull in production may be only temporary. Search for forecasts in the industry. Trade associations use experts that the market relies on.

“Value is the present worth of all the anticipated future benefits to be derived from a property….Prior sales and prior income streams are important only when they parallel the current actions of buyers, thus providing an indication of what may be expected in the future.” Property assessment valuation (3rd ed., p. 16). (2010).

Kansas City, Missouri: International Association of Assessing Officers.

- How much depreciation is already being granted by using the NCDOR Cost Index and Depreciation Schedules?

“Extended Life Expectancy is the increased life expectancy due to seasoning and proven ability to exist. Just as a person will have a total normal life expectancy at birth which increases as he/she grows older, so it is with structures and equipment.” –Marshall Valuation Service, Section 97 page 1, March 2009.

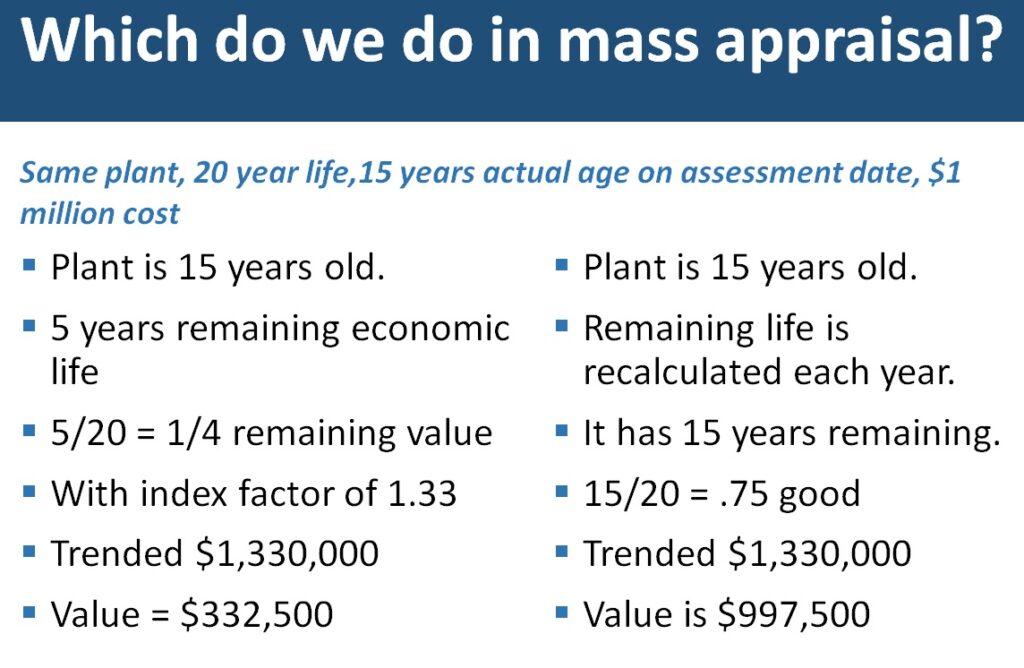

This concept of extended life expectancy is not typically used by mass appraisers of personal property. When we assign, for example a 20-year life, we usually do not change it as the equipment gets older. As each year of age increases, remaining life years decrease by the same. The result of this is that we do not extend remaining economic life as equipment is proven to exist and therefore as equipment gets older, we depreciate it at a higher amount than we otherwise would. The example below demonstrates the concept of extended life expectancy and remaining economic life.

You can see on the right, recalculating remaining economic life each year as equipment proves its ability to exist, results in a higher value than the calculation on the left. We do mass appraisal in North Carolina using the method on the left. From this example, I suggest that in our appraisals we inherently already grant more than just normal functional and physical losses in value. This effect increases as equipment gets older. You probably have equipment in your county that is 60 years old, functioning effectively, but we continue to use a 20 year life for appraisal. We should consider this before reducing a business personal property value.

You can see on the right, recalculating remaining economic life each year as equipment proves its ability to exist, results in a higher value than the calculation on the left. We do mass appraisal in North Carolina using the method on the left. From this example, I suggest that in our appraisals we inherently already grant more than just normal functional and physical losses in value. This effect increases as equipment gets older. You probably have equipment in your county that is 60 years old, functioning effectively, but we continue to use a 20 year life for appraisal. We should consider this before reducing a business personal property value. - Has there been testing for recoverability under FASB 144 and if so, can you see the test information? This will require some web searches, but the information is out there and I’m happy to discuss it more. This "testing" is mainly required for publicly traded companies, but is also sometimes done by accountants for other purposes. FASB establishes standards of financial accounting that govern the preparation of financial reports by nongovernmental entities. FASB 144 refers to the accounting for the impairment of certain assets and refers to the fair value of an asset being the amount at which that asset could be bought or sold in a current transaction between willing parties, that is, other than in a forced or liquidation sale. Does that sound similar to our statutory definition of fair value? There is a lot to learn about this Financial Accounting Board Standard. However, take note of some of the listed examples of events or changes that, should they occur, require businesses to test for recoverability. If they haven't tested, but normally would, or if they are publicly traded, then these events or changes below have not occurred. I have added the underlining in these examples.

- A significant decrease in the market price of a long-lived asset (asset group)

- A significant adverse change in the extent or manner in which a long-lived asset (asset group) is being used or in its physical condition

- A significant adverse change in legal factors or in the business climate that could affect the value of a long-lived asset (asset group), including an adverse action or assessment by a regulator.

- A current-period operating or cash flow loss combined with a history of operating or cash flow losses or a projection or forecast that demonstrates continuing losses associated with the use of a long-lived asset (asset group)

- A current expectation that, more likely than not, a long-lived asset (asset group) will be sold or otherwise disposed of significantly before the end of its previously estimated useful life.