Consulting and updating your revenue manual is the first step of the administrative process for revenue forecasting. At least, that is what I say when I teach revenue forecasting. Of course, when I then turn to the course participants and ask how many of them have revenue manuals in their jurisdiction only one or two raise their hands. In fact, there are some years when no one raises their hand.

Many have never heard of a revenue manual and are surprised to hear that it is step one in a process they do every year! It sounds hard. It sounds daunting. It sounds like something they should probably not start right before budget season. And to the back burner it goes.

In this blog post, I am going to talk about what a revenue manual is, the components, and share some examples. I will also be presenting on this material at the 2021 North Carolina Local Government Budget Association’s Winter Conference and that presentation will be followed be a roundtable discussion of some folks around the state sharing their experience with creating and maintaining revenue manuals. I hope you will be able to join us.

First things first, what is a revenue manual? When teaching MPA students I, somewhere in that first week or so, tell them that a public budget is an encyclopedia of government. It includes everything that government does and typically why. It is the most revealing document about what a government values. I show them an old clip from the 2012 Vice-Presidential election debate of then Vice President Biden saying “Don’t tell me what you value, show me your budget and I will tell you what you value.” Then I make an obligatory snarky comment about I guess the federal government doesn’t value much since they can’t pass a budget. Like our whole-government encyclopedia (i.e., the budget), a revenue manual is an encyclopedia of how government is financed. For those of you who are young enough to have never done a research project in elementary school using only encyclopedias, it is kind of like Wikipedia. It, hopefully, has everything of relevance on that topic—in this case the revenue sources your government relies on to function. While it may not be as revealing of a document as the budget, it is still critical.

More technically, it is a single location for government to catalog their revenues. All revenues should be included. Ideally, each revenue should get its own entry and each one of those entries should contain the same basic information and be formatted the same. It, like your budget, is a technical document. There are many reasons that creating and maintaining a revenue manual is a worthwhile endeavor. First, it allows revenue forecasters and budget analysts (amongst others) to more easily explain the forecast results, assumptions, limitations, and processes to elected officials, managers, and residents. Second, it is an important tool for future forecasts. It is a starting point for revenue forecasting, rather than either leaning on our memory or recollection of assumptions, laws, outcomes, etc or having to go back to recollect and confirm the information and data—it is all right there in the revenue manual. However, it is not just for your benefit.

We often hear from our HR and Org Theory-minded colleagues how important succession planning is. Think of a revenue manual as a tool for what you would need to pass along if your finance officer (or whomever forecasts revenue for your jurisdiction) were to leave tomorrow and someone new to your organization were hired to replace them. What does that person need to know? What are the laws that govern motor vehicle taxes in North Carolina? When did you last go through an assessment cycle? What is the city’s sales tax rate? Trick question! This is why you need to give the new guy a revenue manual! A revenue manual is truly a resource to everyone who touches the budget process, whether it is directly like department heads who are responsible for forecasting their revenues or indirectly like elected officials and the public.

That leads to the next critical question, what all should be included in a revenue manual? Quite a bit. Let’s start with the wish list, that ignores any constraints that may be in place in gathering all of these data points.

The revenue manual wish list:

- A definition and description of the revenue instrument

- Laws authorizing use

- Including any limitations such as TELs and rate caps

- Collection and assessment mechanisms

- Accounting details (including the fund)

- Forecasting techniques

- How the revenue is calculated

- Revenue history

- Details on the recurring (or non-recurring) nature of the revenue source

- Factors that impact the revenue instrument

- And anything else that is helpful to understand that revenue source!

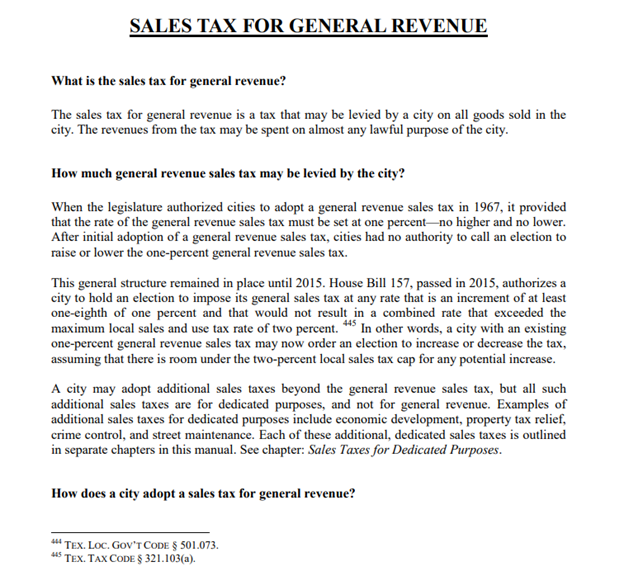

That is a pretty intimidating list. We will get into where to start at the end of this blog, but let’s first dive into some of these areas a bit more. What goes into laws? Of course, there are numerous answers to that question. But for some basics, it can and should include: state statutes and regulations and/or the local ordinance. When relevant it should also list limitations and restrictions, such as rate caps and revenue earmarks. It can also include legal constraints on who is subject to the tax, fees, fines, and penalties. An excellent example as a revenue manual with the “wish list” is a revenue manual made by the Texas Municipal League. Since it is an example for all municipalities in Texas, it does not have the history and specifics to the jurisdiction information but is extremely comprehensive otherwise. For example, see the TML’s discussion of local sales taxes. On page 91 of that document, it discusses sales taxes for general revenue. It defines the tax, discusses what can be levied, describes the process of adoption, how it is collected, the tax base, and much more. It then moves on to sales taxes for property tax relief and the multitude of other local sales tax instruments available in Texas. It has a focus on the legal constraints and processes for the local sales tax.

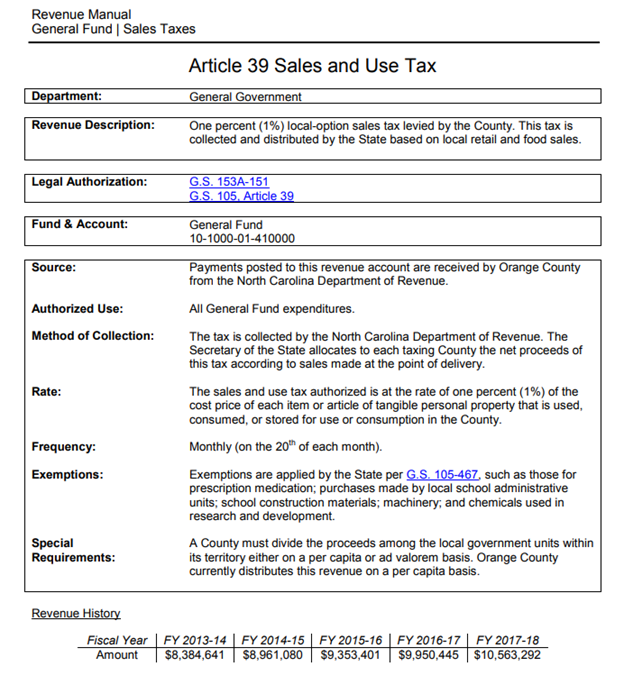

For a more manageable example, and one closer to home, please see Orange County’s revenue manual. It discusses local sales taxes starting on page 10 and similarly to TML’s it breaks them down by article. It links to the statutes authorizing the County to levy the tax, discusses the rate and tax base, and nuances such as the revenue sharing with municipalities. These can all be considered components of the legal structure, but they are also important facets of the financial management of the revenue source. Lastly, unlike the TML example, it presents the revenue history.

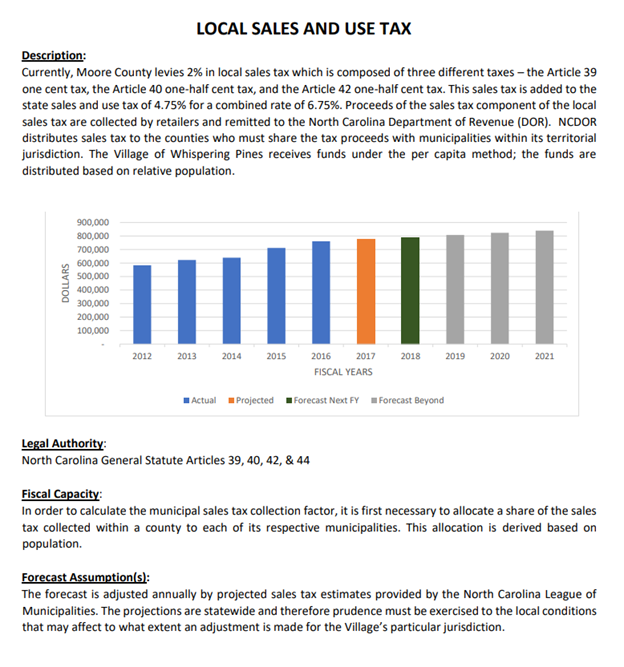

One final example comes from the Village of Whispering Pines. Not only does Whispering Pines provide a straightforward and clear example of a revenue manual, but it also is a great example of a smaller jurisdiction taking on the task and a more streamlined version that many jurisdictions could take on and emulate. Whispering Pines presents information on the local sales tax on page 8 of their revenue manual. Like Orange County they present their historical revenues and take a further step of presenting their forecasts. The Village also presents a description of the revenue source and their forecast assumptions and methods.

These three examples demonstrate distinct approaches that can be taken when crafting a revenue manual. In fact, I believe the introduction to Whispering Pines’ revenue manual sums it up nicely:

This Village of Whispering Pines Revenue Manual serves as a tool to define, assess and determine the fiscal capacity and fiscal health of the Village of Whispering Pines. A community’s fiscal capacity stems directly from its tax and revenue base. The Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the Village.

This Revenue Manual is an in-depth view of the Village’s revenue sources and its purpose is to provide detailed information of the types of revenue that the Village of Whispering Pines utilizes to provide public services to the community. The Village relies on a variety of revenue sources in order to finance the cost of services provided to its residents. (Page 2)

These examples help to answer the ultimate question that many of you have—where should I start? Of course, some of the answer depends on where you want to finish and how comprehensive you want your revenue manual to be. That being said here are my suggestions of where to start.

First, start with your major revenue sources. For the vast majority of counties and municipalities that is going to mean property and sales taxes. For many of you, it will also mean utilities and occupancy taxes. Decide on those “major” revenue sources and then decide what all you want to collect on them, at least to begin with. This list should at least include: description, authorization, history of revenues, and rates. That list will also depend on the revenue instrument. For example, with property taxes you would also want to make sure to include the assessment cycle and how it is calculated.

Second, seek out existing resources. There are a lot of great resources available on North Carolina revenues and there is no reason to reinvent the wheel. I suggest going to Coates Canons where many of my legal colleagues discuss revenues in North Carolina with an emphasis on the legal structures and nuances. There are also chapters on revenues in texts like County and Municipal Government in North Carolina, Introduction to Local Government Finance, and Budgeting in North Carolina Local Governments. And, of course, looking at the revenue manuals of fellow county and municipal governments in North Carolina.

Third, think about what historical data and information you would like to include and add it in. Revenues are a must, but I would also encourage you to add other important information such as rate changes and re-assessment dates. You should be thinking “what information would be helpful for someone not familiar with this data to understand it?”

My final recommendation is to get help! This is a great project for an MPA intern! In fact, Orange County notes in their preface that an intern was important in crafting their revenue manual.

Good luck and just remember it is a process and the first version does not have to be the final version!

References:

- Morgan, D., Robinson, K. S., Strachota, D., & Hough, J. A. (2017). Budgeting for local governments and communities. Routledge.

- Orange County, NC Department of Finance & Administrative Services. “Revenue Manual.” https://www.orangecountync.gov/DocumentCenter/View/6027/Revenue-Manual

- Texas Municipal League. “Revenue Manual for Texas Cities.” https://www.tml.org/DocumentCenter/View/68/Texas-Municipal-League-Revenue-Manual-for-Texas-Cities-PDF

- Village of Whispering Pines, NC Finance Office. 2017. “Revenue Manual.” https://whisperingpinesnc.net/files/documents/RevenueManual1316100929032818AM.pdf

November 3, 2021 at 10:02 am

Nice comprehensive post, Whitney.