Yup, you guessed it, today’s blog post is on revenue forecasting! My current blog series is about some of the non-legal finance issues that are out there and revenue forecasting, while required by law, is a really important one! There are many people that are involved with revenue forecasting in local governments. While many outside of government may just assume that there is some accountant or budget wonk sitting in a back room who is somehow magically able (or has some very scientific formula) to predict how much money is going to be coming in next year, we know better.

There are many reasons to forecast revenues including planning for the future (are we going to have enough money coming to support our expenditures in five years) and to balance this year’s budget, but in North Carolina local governments are also required by law to forecast revenues. Our forecasted revenues set the parameters on the budget, they define how much we can spend this year and may cause policy choices on both the expenditure and finance side (like setting the property tax rate).

This is why it is explicitly required in the Local Government Budget and Fiscal Control Act or simply the Fiscal Control Act. The Fiscal Control Act requires that the budget is balanced and that the estimated revenue for the following year, used to create the balanced budget, be reasonable, reliable, and justifiable. The question is, how do we do that?

This is why it is explicitly required in the Local Government Budget and Fiscal Control Act or simply the Fiscal Control Act. The Fiscal Control Act requires that the budget is balanced and that the estimated revenue for the following year, used to create the balanced budget, be reasonable, reliable, and justifiable. The question is, how do we do that?

In this blog post I am going to discuss forecasting methods broadly, if this is something you are more interested in and you want more details (and math!) please see my chapter in the Introduction to Local Government Finance textbook.

First, of all what do we need to successfully forecast our revenues? We need: data, institutional insight, and judgement. We need data on the revenues we have collected in the past, policy changes, changes to our tax base, and whatever else we think may be important to know about past revenues and future revenues. For example, beyond just property tax collections it is important to have data on property tax rate changes, reassessment cycles, etc.

Data is foundational, but without institutional insight it would be easy to misinterpret that data. Institutional insight and knowledge helps a forecaster know what data needs to be collected, what effect changes have had on your community, what population or demographic changes may be occurring, whether firms are entering or exiting, etc. Institutional insight provides the context for the data. In a course I was teaching, I had the opportunity to talk with a budget officer from Fayetteville and we were talking about unexpected shocks to budgets. She mentioned how the federal government shut down that occurred in 2013 really hit them hard because of the importance of Fort Bragg to their community. They were affected by the shutdown in ways that most jurisdictions outside of metro D.C. were not. If you had no context and were looking at their revenue receipts for that period and comparing them to other jurisdictions you would not only be confused but you would also let that shock affect your forecast in inappropriate ways.

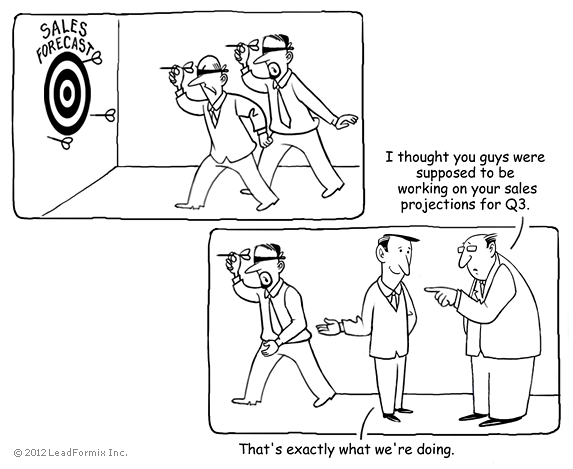

Lastly, you have to always use your judgement. You need to make sense of the numbers, look at the trends, and not rely exclusively on the numbers spit out of models. I sometimes refer to this as the “gut check.” You can use real numbers and reasonable forecasting methods and get unrealistic forecasts. There are a lot of reasons this may happen and we are going to discuss some of them below!

There are two main categories of forecasting methods: qualitative and quantitative.

Qualitative forecasting relies on expert judgement. The experts can be internal (like budget directors) or external (like local economists). This is extremely common and can be very reliable when the expert understands the revenue source, the economy, and the community. Can’t decide on just one expert? You can also use a panel of experts who bring different knowledge and perspectives to the process. This often means internal experts as well as economists, business owners, bankers, etc. There are many strengths to qualitative forecasting such as it is typically low cost, straightforward, and not too data intensive. ***Note: This does not mean that our experts do not use data though!*** However, it has its share of weaknesses too. You need to identify the correct experts, it is not as transparent a process, and it is hard to avoid forecaster bias. Forecaster bias comes in many shapes and sizes but an example of it is that your expert remembers last time there was a downturn and it took your community 5 years to get back to previous sales tax collections, never mind that the previous economic downturn was the Great Recession and the next downturn will likely (hopefully!) be much less dramatic. Or they know that this new box store coming in is going to generate tons of revenue, they just know it!

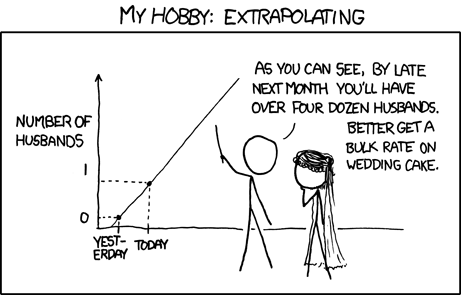

Quantitative judgement relies on data very heavily and there are numerous ways it can be accomplished. For some tax sources, like property taxes, they can be forecasted through formulas because you have all the data you need (like tax base, rate, and collection rate) to calculate it. Unfortunately this information is not available for the majority of taxes and fees. A common method of quantitative forecasting is trend analysis, where the forecaster uses previous collections (and the changes from year to year) to estimate future collections. There are many ways to forecast using trends including applying the average growth over the period to the previous year's revenue. The issue you here is that trend analysis is always backward looking and will lag behind changes to the economy.

A final way that is more common in larger jurisdictions is causal modeling where not just previous revenue is used, but also other economic drivers. The advantage is that it can be forward looking and it incorporates the “why” of changing revenue collections. It requires a lot of data though and for most local governments that data is not available, at least not for the most recent time periods. And when it comes to data you should always remember GIGO: Garbage in, Garbage out.

So how do we choose? Well resources are the first hurdle. What capacity do you have on staff (not just skill set but time)? Do you have the money to hire consultants? Do you have the data? The second consideration is to think about the revenue being forecasted, you should not be using the same (quantitative) forecasting technique for all your revenue sources. ***See the book chapter for more on this.*** The third consideration is what works on previous data? I suggest you forecast for previous years using a few different methods. You know what the actual revenue collections are, so you will be able to identify which quantitative methods work best for different revenue sources.

Final thoughts on revenue forecasting.

- All forecasts are wrong. The goal is to minimize how wrong they are.

- Be cautious, but not too cautious. It is prudent to air on the conservative side of forecasting but too conservative and you are either taxing people too much or you are missing opportunities by not budgeting your revenues.

- Expert judgement should always be incorporated, even when doing quantitative forecasting. The gut check of “does this make sense” is valuable. I suggest you graph your estimate against the previous years to eyeball your forecast to help inform that gut check.