There are many certification programs involved with property tax. I suggest that every NC property tax student be familiar with which organizations provide certifications, credit hours, and the requirements of those organizations. A certification or designation is required by law for some positions. Two are required in the assessor’s office. If you are one of the 100 appointed county assessors in North Carolina or a county appraiser, you must be certified by the NC Department of Revenue. Becoming and being a certified assessor or appraiser includes requirements for initial certification (certifying education) and also follow-up requirements for continuing education. If you represent yourself as a real estate appraiser but do not fill one of the two positions above, NC law requires your certification to be through the NC Appraisal Board. All other certification programs for property tax are not legally required in NC law but may be required by your employer or by your association. Perhaps you’re not currently in a position that is required to be certified but your future could lead you in that direction. Regardless, I think you should maintain your course records for attendance and successful completion of property tax courses. I have recognized uncertainty in this area over the years and it seems to be more so in recent times. I hope this post is a way to help bring us back to certainty. Continue reading

Page 2 of 10

Guest Contributors: Hai (David) Guo and Can Chen

What is the most significant fiscal challenge for the municipal governments facing the unexpected outbreak of the COVID-19 pandemic? It is no surprise that Florida city managers placed the forecasts for the pandemic’s impact on local revenues as the top priority, as local governments are revenue-driven entities. The tradeoff between revenue growth and stability has always been a concern for local governments. With procyclical fiscal policy, local governments usually face abrupt revenue shortfalls and high demand for public service during economic recession. The COVID-19 pandemic-induced recession is no exception. Furthermore, there is tremendous uncertainty regarding the duration of the pandemic, the magnitude and requirement of federal government aid, and the public’s behavioral change.

Continue reading

To those who have already donated: on behalf of the faculty and staff at the School of Government, we thank you for being a part of GiveUNC. We are grateful for your support of both the School and the state of North Carolina.

For the entirety of its 90 years of existence, the School of Government’s mission has been focused on the people of North Carolina. Through our commitment to offering high-quality education, advising, and support to public officials across the state, we improve the lives of North Carolinians. We firmly believe this work is more critical than ever.

Continue reading

Today is GiveUNC, the annual university-wide day of giving at UNC-Chapel Hill. Support from this event has a tremendous impact on the School of Government’s ability to continue providing advising, education, and support to North Carolina public officials. Gifts of all sizes make a meaningful difference. We hope you will consider making a gift today.

And as many of you know, David Ammons is set to retire at the end of the spring. David has been a critical resource to the state and to the NCLGBA – teaching important programs around performance measurement and management, doing sessions at our conferences, and consulting with individual communities. A scholarship honoring David’s commitment and service to the state and UNC MPA has been established. If you would like to donate to support this scholarship, you can do so here.

Continue reading

Recently I participated in a webinar for Kenan Flagler’s Tax Center. It covers state responses to the pandemic and policies being considered. While it is not focused on North Carolina or local governments, I think there is still much in there that is likely of interest to you all. Especially because we all know that what happens at the state level impacts the local level.

And my co-presenters (their bios are at the bottom) were amazing! One was named “The Most Influential Person on the Planet in State and Local Tax” by State Tax Notes and the other was identified by State Tax Notes as the “single most influential person in state taxation” and named as the publication’s inaugural Person of the Year.

The webinar is available here.

Continue reading

I have been having a great deal of conversations with folks across the state about what is going on with their sales taxes (and occupancy and food and beverage taxes). What has happened versus what was expected for FY21 and what they are thinking about for FY22 now that local governments are starting to begin their budget processes. I thought it might be useful to share some of the questions I have been getting and my answers to them and some of my broader thoughts about sales taxes and the pandemic, though it is no crystal ball. I am going to structure it like a q&a. I am not covering everything here and please reach out if there is more than I can help with.

- Q: Our sales taxes are recovering quickly, what are you seeing other places in the state?

- A: We are seeing that sales taxes have recovered more quickly than most people anticipated. That is great news, but I think a dose of caution should accompany it. First, we see a bump starting in in the June collections (so sales for the month of May) where it went from down 13.3% year-over-year to down 4% year-over-year and then by July (so June sales) it was up year-over-year by 10.75%. So that is all really promising, but we have to keep a few things in mind. 1) That is right when the state moved into Phase 2 and there may have been pent up demand. 2) That is when we have more generous unemployment benefits and federal stimulus, so people had more disposable income than they might otherwise have had. 3) Some people were deferring payments on rent and/or utilities, so they had less income than it looked like from their spending in that period. Also, that trend is not universal. Some areas are doing much better and others are having a slower recovery.

In a previous blog post, The COVID-19 Crisis and How North Carolina Local Governments are Budgeting for It, I laid out the results of a survey that the NCLM and the NCLGBA had conducted to counties and municipalities across the state in April. In this week’s blog post I am going to provide an overview of an updated survey that was send out in May. This survey had fewer respondents, but also provides more up-to-date information about the strategies and plans that local governments in North Carolina have, with another full months of information and better understanding of how COVID-19 is impacting their jurisdiction.

Continue reading

As governments are nearing the end of budget season in these uncertain times we want to make sure you all are aware of some of the resources available from the School of Government and our partners. There are many COVID-19 resources at the UNC SOG dedicated Microsite.

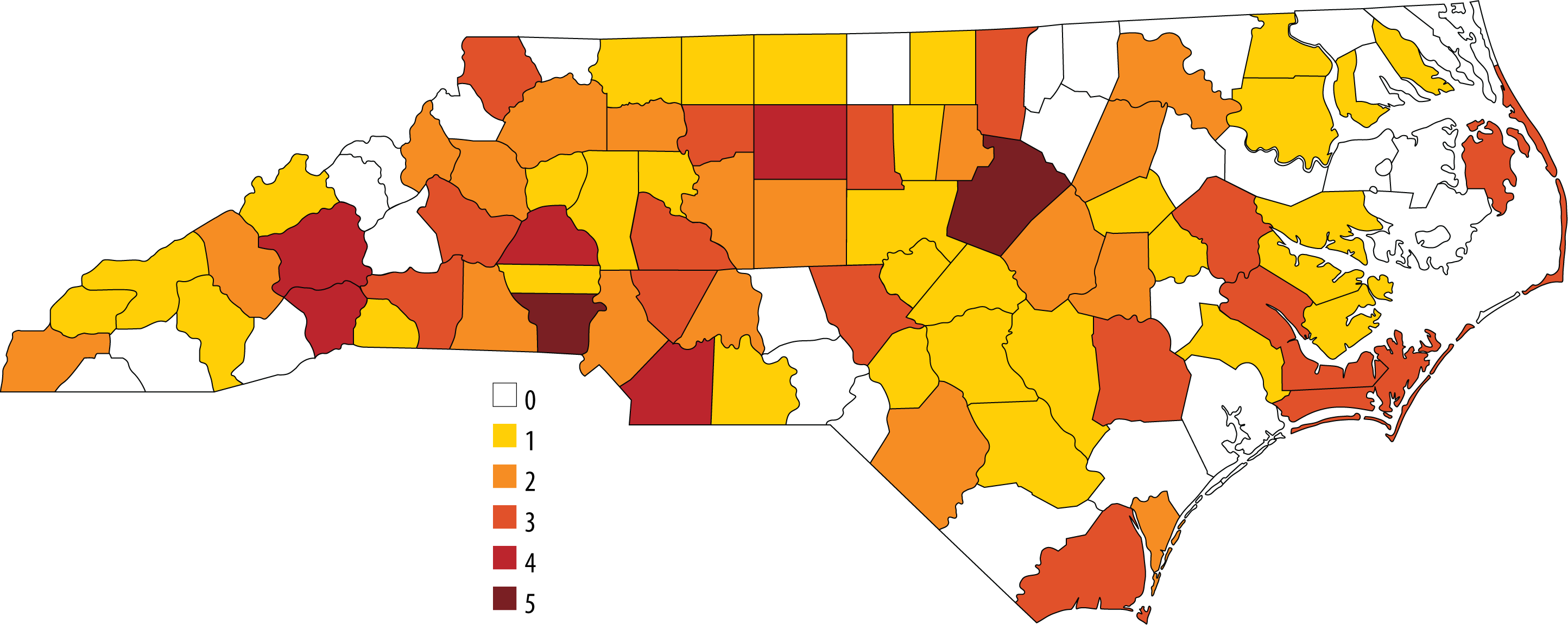

Recently the North Carolina League of Municipalities (NCLM) and the North Carolina Local Government Budget Association (NCLGBA) partnered on a survey of county and municipal governments across the state to better understand how local governments are budgeting for FY21. There are 142 responses. 29 are from counties and 113 are from municipalities. See the map below to see the number of jurisdictions from each county area (total of the county and municipal responses).

As a response to the current Covid-19 pandemic, on March 26, 2020, the Governmental Accounting Standards Board (GASB) added a fast-track project to their agenda. This project is a proposal to consider the delay of required implementation of pending statements and related Implementation Guide provisions that were initially set to be effective for fiscal years that begin on or after June 15, 2018. This would encompass several significant statements such as GASB Statement No. 84, Fiduciary Activities, and GASB Statement No. 87, Leases. Specifically, an Exposure Draft is expected in April with the final guidance anticipated in May.

© 2024 Copyright,

The University of North

Carolina at Chapel Hill.

Theme by Anders Noren — Up ↑